- Buy Crypto

- Markets

Futures

Futures- Spot

- Copy Trade

Earn

Earn- More

a16z: How will stablecoins eat into the payments industry? What happens after that?

Original title: How stablecoins will eat payments, and what happens next

Original author: Sam Broner, a16z crypto investment partner

Original translation: 0xjs, Golden Finance

Today's payments landscape is dominated by gatekeepers who charge high fees, undercut the profitability of every business they touch, and justify those fees in the name of ubiquity and convenience — while they stifle competition and limit the creativity of builders.

Stablecoins can do better.

Stablecoins have lower fees, more competition among payment providers, and wider accessibility. Because stablecoins reduce transaction costs to almost zero, they can free businesses from the friction of existing alternatives. Adoption of stablecoins will start with businesses most affected by current payment methods, a process that will disrupt the payments industry.

Stablecoins have become the cheapest way to transfer dollars. Last month, 28.5 million unique stablecoin users sent over 600 million transactions. Stablecoin users are found in nearly every country and use stablecoins because they offer a safe, cheap, and inflation-resistant way to save and spend. Aside from cash and gold, stablecoins are the only widely adopted payment method that can operate without gatekeepers such as banks, payment networks, or central banks. At the same time, stablecoins are permissionless, programmable, scalable, and integrable—anyone can help build a stablecoin payment platform on top of a stablecoin payment rail.

This disruption may take time, but it may happen faster than many expect. Businesses such as restaurants, retailers, enterprises, and payment processors will benefit the most from stablecoin platforms, with significantly higher profit margins. This demand will drive adoption, and as stablecoin adoption continues to increase, the other benefits of stablecoins—permissionless composability and improved programmability—will bring more benefits to on-chain users, businesses, and products. I’ll share more whys and hows below, but first some background on the payments industry.

Payment Tracks

• Payment Channels: The technology, rules, and networks that process transactions

• Payment Processors: Operators on the payment rails that facilitate transactions

• Payment Service Providers: Entities that provide access to payment systems to end users or other systems

• Payment Solutions: Products provided by payment service providers

• Payment Platforms: A suite of interrelated payment solutions across providers, processors, and rails

Payments Industry Background

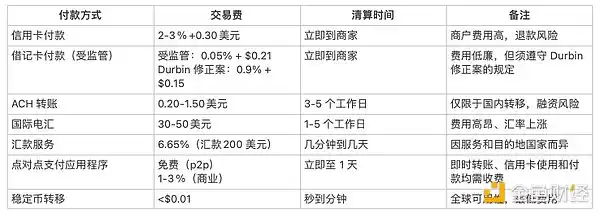

The size of the payments industry cannot be underestimated. In 2023, the global payments industry processed 3.4 trillion transactions worth $1.8 trillion and generated $2.4 trillion in revenue. In the United States alone, credit card payments accounted for $5.6 trillion and debit card payments accounted for $4.4 trillion.

Despite the industry’s ubiquity and scale, payment solutions remain expensive and complex, and payment apps are often shielded from the consumer experience. For example, while peer-to-peer payment app Venmo may look simple on the front end, on the back end, the product hides a maze of bank integrations, debit card vulnerabilities, and countless compliance obligations. Payment solutions are often interdependent, which adds to the complexity, and people still use a variety of payment methods: cash, debit cards, credit cards, peer-to-peer payment apps, ACH (Automated Clearing House), checks, etc.

The four main metrics for payment products are timeliness, cost, reliability, and convenience.

Consumers prioritize questions like “How much will I pay?” Merchants ask “Will I get paid?” But in fact, all four metrics are essential for both parties.

Ever since businesses had to find fraudulent credit cards in physical ledgers, waves of innovation have continuously improved the payment experience. Each wave of innovation has brought faster, more reliable, more convenient, and cheaper payment methods, which in turn has led to an increase in transaction volume and the amount spent.

But many customers are still not enjoying modern services, or are underserved. For merchants, credit cards are expensive, directly eating into their profits. Despite growing adoption of real-time payments (RTP), U.S. bank transfers are still too slow, taking days. And peer-to-peer applications are region- and network-specific, making transfers between ecosystems slow, costly, and complex.

While businesses and consumers have come to expect more sophisticated functionality from payment platforms, not all users benefit from existing solutions. In fact, most users pay too much in fees and don’t use all of the bundled payment products. But they accept the current state of affairs.

Where Stablecoins Fit In

The key to stablecoins disrupting the industry is the failure of existing payment solutions (high cost, low availability, or high friction), and the fact that bundled products of payment solutions (including identity, lending, compliance, fraud protection, and bank integration) are least necessary.

Take remittances as an example. It was born out of desperation. Many remittance users are underbanked and use highly fragmented banking services. As a result, these users see little value in native integrations between traditional payments and banking services. Stablecoin payments offer instant finality, low costs, and no middlemen, which are structural advantages for any payment user or builder. After all, with stablecoins, it costs less than $0.01 to send $200 from the United States to Colombia, but $12.13 on traditional corridors. (Remittance users need to send money home regardless of transaction costs, but will benefit greatly from lower fees.)

International commercial payments, especially for small businesses in emerging markets, also face high fees, slow processing times, and low bank acceptance. For example, a payment between a Mexican apparel manufacturer and a Vietnamese textile manufacturer will involve four or more intermediaries – local bank, foreign exchange, correspondent bank, correspondent bank, foreign exchange, local bank. Each intermediary charges a percentage and there is a risk of middleman bankruptcy.

Fortunately, these transactions occur between partners with a regular relationship. With stablecoins, Mexican payers and Vietnamese payees can experiment and eliminate slow, bureaucratic, and expensive intermediaries. They may have to work hard to find local channels and workflows, but in the end they can enjoy faster, cheaper transactions and more control over the payment process.

Small-value transactions (especially low-fraud face-to-face transactions, such as those conducted in restaurants, coffee shops, or corner stores) are also a promising opportunity. These businesses are cost-sensitive due to their low profit margins, so the 15-cent transaction fee charged by payment solutions has a big impact on their profitability.

For every $2 a customer spends on a cup of coffee, only $1.70 to $1.80 goes to the coffee shop, with the remaining nearly 15% going to the credit card company—just for facilitating the transaction. But credit cards are here for convenience: neither the consumer nor the store needs additional features to justify the charges. Consumers don’t need fraud protection (they’re just getting a cup of coffee) or loans (the coffee was only $2). And coffee shops have limited compliance and bank integration needs (they typically use integrated restaurant management software or none at all). So if there’s a cheap, reliable alternative, these businesses will take advantage of it.

Cheaper Payments Improve Profitability

Current payment system transaction fees directly hurt the bottom line for many businesses. Lowering these fees would provide a huge boost to profitability. The first shoe has already dropped: Stripe announced they will charge 1.5% on stablecoin payments, 30% less than what they charge for credit card payments. To support this effort, Stripe announced the acquisition of Bridge.xyz for approximately $1 billion.

Wider adoption of stablecoins would significantly improve profitability for many businesses—not just small businesses like coffee shops or restaurants. Let’s look at the financials for three public companies in fiscal 2024 to get a rough idea of the impact of reducing payment processing rates to 0.1%. (For simplicity, this assessment assumes that businesses pay a 1.6% hybrid payment processor cost and that on- and off-ramps have minimal costs. More on this below.)

· Walmart, with $648 billion in annual revenue, could pay $10 billion in credit card fees and make $15.5 billion in profit. Do the math: Given the elimination of payment fees and Walmart's profitability, its valuation (controlling for all other factors) could increase by more than 60% just through a cheaper payment solution.

· Chipotle is a fast-growing fast-food restaurant with $9.8 billion in annual revenue. It makes $1.2 billion in profit each year, of which it pays $148 million in credit card fees. Just by reducing fees, Chipotle could increase profitability by 12%—an astonishing number not available elsewhere on its income statement.

· National grocer Krogers has the lowest margins and therefore makes the most money. Surprisingly, Krogers’ net revenue and payment costs may be nearly equal. Like many grocery stores, its profit margin is less than 2%, which is less than the fees businesses pay to process credit card payments. With stablecoin payments, Krogers’ profits could double.

How will Walmart, Chipotle, and Krogers reduce transaction fees with stablecoins? First, consider an idealized scenario: consumers will not accept stablecoins all at once, and there will still be considerable fees until stablecoins gain enough acceptance, especially when starting and stopping use. Second, both retailers and payment processors oppose high-fee payment solutions. Payment processors are also low-margin businesses that give up most of their profits to credit card networks and issuing banks. When payment processors process transactions, most of their fees are passed on to payment networks. So when Stripe handles the online retail checkout process, they take a 2.9% cut of the total transaction and a $0.30 fee, but they pay more than 70% to Visa and the issuing bank. As more payment processors like Block- formerly Square, Fiserv, Stripe, and Toast adopt stablecoins to improve their profit margins, they will make stablecoins more accessible to more businesses.

Stablecoins have low fees and no network gatekeeper fees to pay. This means payment processors earn much higher margins on revenue from stablecoin transactions. Higher margins could lead payment processors to support and encourage more businesses and use cases to use stablecoins. But as payment processors begin to adopt stablecoins, expect stablecoin payment fees to compress over time: Stripe’s 1.5% fee is likely to fall.

Next Steps: Mass Consumer Adoption

Today, stablecoins are a new permissionless way to send and store money. Entrepreneurs are already building solutions to turn stablecoin rails into stablecoin platforms. As with previous innovations, adoption will occur gradually, starting at the fringes of consumer demand, then forward-thinking businesses, until the platform matures enough to meet the needs of everyday users and cautious businesses. Three trends will drive more mainstream enterprise adoption of stablecoins.

1. Increase back-end integration through stablecoin aggregation

Stablecoin aggregation (the ability to monitor, guide, and integrate stablecoins) will soon be integrated into payment processors such as Stripe. These aggregation products enable businesses to process payments at a much lower cost than current mechanisms without major process or engineering changes. Consumers may end up with cheaper products without knowing it, because invoices, payrolls, and subscriptions have lower structural costs by default.

Many of these stablecoin aggregation businesses have begun to attract customers who want instant settlement, low-cost, and widely available business-to-business or business-to-consumer payments. By integrating stablecoins in the backend, businesses will benefit from the advantages of stablecoins—without interrupting or reducing the quality of service that users expect from payment providers, while the adoption of stablecoins will increase.

2. Improve the enterprise entry process and increase shared incentives

The stablecoin business is becoming more and more mature in bringing end users into the chain by sharing incentives and improving entry solutions.

Entry is becoming cheaper, faster, and more ubiquitous, making it easier for users to get started with cryptocurrencies. At the same time, more and more consumer applications support cryptocurrencies, allowing users to benefit from the expanded stablecoin ecosystem—without adopting new applications or user behaviors. Popular applications such as Venmo, ApplePay, Paypal, CashApp, Nubank, and Revolut allow their customers to use stablecoins.

Moreover, companies are more motivated to use these channels to integrate stablecoins and deposit funds in stablecoins. Fiat-backed stablecoin issuers such as Circle, Paypal, and Tether are sharing profits with ordinary businesses, just as Visa shares profits with United and Chase for signed credit card users. Such cooperation and integration benefit stablecoin issuers because they can create a larger pool of assets to earn returns. But they can also benefit businesses that successfully convert users from credit cards to stablecoins. These businesses can now earn a portion of the revenue generated by the funds their products generate, a business model that is usually only available to banks, fintech companies and gift card issuers that make money from user float.

3. Improve regulatory clarity and availability of compliance solutions

When businesses are confident in the regulatory environment, they are more likely to adopt stablecoins. While we have not yet seen comprehensive global regulation of stablecoins, many jurisdictions have issued rules and guidance on stablecoins, allowing entrepreneurs to start the hard work of building compliant, user-friendly businesses.

For example, the EU's Markets in Crypto-Assets Regulation (MiCA) sets rules for stablecoin issuers, including prudential and behavioral requirements. Since the stablecoin provisions came into effect earlier this year, the regulation has significantly changed the European stablecoin market.

Despite the current lack of a stablecoin framework in the United States, policymakers from both parties are increasingly recognizing the need for effective stablecoin legislation. Such regulation needs to ensure that issuers fully back their tokens with high-quality assets, have their reserves audited by third parties, and take comprehensive measures to combat illegal financial activities. At the same time, legislation needs to preserve the ability of creators to create decentralized stablecoins, reduce user risks by eliminating intermediaries, and take advantage of decentralization.

These policy efforts will get companies across industries to consider moving from traditional payment methods to stablecoin infrastructure. While compliance solutions are unattractive, everyone who adopts stablecoins helps prove to incumbents that stablecoins are a reliable, secure, regulated, and improved solution to traditional payment problems.

As stablecoins gain popularity, the platform’s network effects will grow stronger. While it may still be a few years before stablecoins can be used at point-of-sale or as a replacement for bank accounts, as the number of stablecoin users grows, stablecoin-centric solutions will become more mainstream and more attractive to consumers, businesses, and entrepreneurs.

Trend: Why Stablecoins Will Continue to Improve

As adoption progresses, the product itself will continue to improve. The web3 community is celebrating stablecoin adoption for good reason: stablecoins are climbing the value innovation S-curve thanks to years of investment in infrastructure and on-chain applications. As infrastructure improves, on-chain applications become more abundant, and on-chain networks grow, stablecoins will become more attractive to users. This will happen in two ways.

First, the painstaking engineering of crypto infrastructure has made stablecoin payments of less than a cent possible. Future investments will continue to make transactions cheaper and faster. At the same time, stablecoin aggregation and an improved onboarding experience are only possible through better wallets, bridges, deposits and withdrawals, developer experience, and AMMs.

This technological foundation provides increasing incentives for entrepreneurs to build stablecoins that provide a better developer experience, a rich ecosystem, broad applications, and permissionless composability of on-chain currencies.

Second, stablecoins unlock new user scenarios through the permissionless composability of on-chain currencies. Other payment platforms have gatekeepers that force entrepreneurs to work with extraction networks, such as costly intermediaries in credit card transactions or international payments. But stablecoins are self-custodial and programmable, lowering the threshold for creating new payment experiences and integrating value-added services. Stablecoins are also composable, allowing users to benefit from increasingly powerful on-chain applications and increasing competition. For example, stablecoin users have benefited from DeFi, on-chain subscriptions, and social applications.

Conclusion

Stablecoins can lead us into a world of free, scalable, and instant payments. As Stripe CEO Patrick Collison said, stablecoins are "room temperature superconductors for financial services." They will enable businesses to pursue new opportunities that would otherwise not be able to withstand the burden of existing payment channels or the friction of traditional gatekeepers.

In the short term, stablecoins will have a structural change to financial products as payments become free and open. Incumbent payment companies will seek new ways to monetize, either by taking a percentage of revenue or by selling services that are complementary to this newly commoditized platform. As these traditional businesses recognize the changing landscape, entrepreneurs will create new solutions that help these businesses leverage stablecoins.

In the long run, as stablecoins become more common and the technology advances, startups will seize the opportunities presented by a world of feeless, frictionless, and instant payments. These startups will be founded today, unlocking new and unexpected scenarios and further democratizing the opportunities afforded by the global financial system.

Acknowledgements: Special thanks to Tim Sullivan, Aiden Slavin, Eddy Lazzarin, Robert Hackett, Jay Drain, Liz Harkavy, Miles Jennings, and Scott Kominers for their thoughtful feedback and suggestions that made this article possible.

You may also like

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.

Wall Street's Hottest Trades See Exodus

Vitalik Discusses Ethereum Scaling Path, Circle Announces Partnership with Polymarket, What's the Overseas Crypto Community Talking About Today?

Believing in the Capital Markets - The Essence and Core Value of Cryptocurrency

Polymarket's 'Weatherman': Predict Temperature, Win Million-Dollar Payout

$15K+ Profits: The 4 AI Trading Secrets WEEX Hackathon Prelim Winners Used to Dominate Volatile Crypto Markets

How WEEX Hackathon's top AI trading strategies made $15K+ in crypto markets: 4 proven rules for ETH/BTC trading, market structure analysis, and risk management in volatile conditions.

A nearly 20% one-day plunge, how long has it been since you last saw a $60,000 Bitcoin?

Raoul Pal: I've seen every single panic, and they are never the end.

Key Market Information Discrepancy on February 6th - A Must-Read! | Alpha Morning Report

2026 Crypto Industry's First Snowfall

The Harsh Reality Behind the $26 Billion Crypto Liquidation: Liquidity Is Killing the Market

Why Is Gold, US Stocks, Bitcoin All Falling?

Key Market Intelligence for February 5th, how much did you miss out on?

Wintermute: By 2026, crypto had gradually become the settlement layer of the Internet economy

Token Cannot Compound, Where Is the Real Investment Opportunity?

February 6th Market Key Intelligence, How Much Did You Miss?

China's Central Bank and Eight Other Departments' Latest Regulatory Focus: Key Attention to RWA Tokenized Asset Risk

Foreword: Today, the People's Bank of China's website published the "Notice of the People's Bank of China, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration for Market Regulation, China Banking and Insurance Regulatory Commission, China Securities Regulatory Commission, State Administration of Foreign Exchange on Further Preventing and Dealing with Risks Related to Virtual Currency and Others (Yinfa [2026] No. 42)", the latest regulatory requirements from the eight departments including the central bank, which are basically consistent with the regulatory requirements of recent years. The main focus of the regulation is on speculative activities such as virtual currency trading, exchanges, ICOs, overseas platform services, and this time, regulatory oversight of RWA has been added, explicitly prohibiting RWA tokenization, stablecoins (especially those pegged to the RMB). The following is the full text:

To the people's governments of all provinces, autonomous regions, and municipalities directly under the Central Government, the Xinjiang Production and Construction Corps:

Recently, there have been speculative activities related to virtual currency and Real-World Assets (RWA) tokenization, disrupting the economic and financial order and jeopardizing the property security of the people. In order to further prevent and address the risks related to virtual currency and Real-World Assets tokenization, effectively safeguard national security and social stability, in accordance with the "Law of the People's Republic of China on the People's Bank of China," "Law of the People's Republic of China on Commercial Banks," "Securities Law of the People's Republic of China," "Law of the People's Republic of China on Securities Investment Funds," "Law of the People's Republic of China on Futures and Derivatives," "Cybersecurity Law of the People's Republic of China," "Regulations of the People's Republic of China on the Administration of Renminbi," "Regulations on Prevention and Disposal of Illegal Fundraising," "Regulations of the People's Republic of China on Foreign Exchange Administration," "Telecommunications Regulations of the People's Republic of China," and other provisions, after reaching consensus with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, and with the approval of the State Council, the relevant matters are notified as follows:

(I) Virtual currency does not possess the legal status equivalent to fiat currency. Virtual currencies such as Bitcoin, Ether, Tether, etc., have the main characteristics of being issued by non-monetary authorities, using encryption technology and distributed ledger or similar technology, existing in digital form, etc. They do not have legal tender status, should not and cannot be circulated and used as currency in the market.

The business activities related to virtual currency are classified as illegal financial activities. The exchange of fiat currency and virtual currency within the territory, exchange of virtual currencies, acting as a central counterparty in buying and selling virtual currencies, providing information intermediary and pricing services for virtual currency transactions, token issuance financing, and trading of virtual currency-related financial products, etc., fall under illegal financial activities, such as suspected illegal issuance of token vouchers, unauthorized public issuance of securities, illegal operation of securities and futures business, illegal fundraising, etc., are strictly prohibited across the board and resolutely banned in accordance with the law. Overseas entities and individuals are not allowed to provide virtual currency-related services to domestic entities in any form.

A stablecoin pegged to a fiat currency indirectly fulfills some functions of the fiat currency in circulation. Without the consent of relevant authorities in accordance with the law and regulations, any domestic or foreign entity or individual is not allowed to issue a RMB-pegged stablecoin overseas.

(II)Tokenization of Real-World Assets refers to the use of encryption technology and distributed ledger or similar technologies to transform ownership rights, income rights, etc., of assets into tokens (tokens) or other interests or bond certificates with token (token) characteristics, and carry out issuance and trading activities.

Engaging in the tokenization of real-world assets domestically, as well as providing related intermediary, information technology services, etc., which are suspected of illegal issuance of token vouchers, unauthorized public offering of securities, illegal operation of securities and futures business, illegal fundraising, and other illegal financial activities, shall be prohibited; except for relevant business activities carried out with the approval of the competent authorities in accordance with the law and regulations and relying on specific financial infrastructures. Overseas entities and individuals are not allowed to illegally provide services related to the tokenization of real-world assets to domestic entities in any form.

(III) Inter-agency Coordination. The People's Bank of China, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of virtual currency-related illegal financial activities.

The China Securities Regulatory Commission, together with the National Development and Reform Commission, the Ministry of Industry and Information Technology, the Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the State Administration of Foreign Exchange, and other departments, will improve the work mechanism, strengthen coordination with the Cyberspace Administration of China, the Supreme People's Court, and the Supreme People's Procuratorate, coordinate efforts, and overall guide regions to carry out risk prevention and disposal of illegal financial activities related to the tokenization of real-world assets.

(IV) Strengthening Local Implementation. The people's governments at the provincial level are overall responsible for the prevention and disposal of risks related to virtual currencies and the tokenization of real-world assets in their respective administrative regions. The specific leading department is the local financial regulatory department, with participation from branches and dispatched institutions of the State Council's financial regulatory department, telecommunications regulators, public security, market supervision, and other departments, in coordination with cyberspace departments, courts, and procuratorates, to improve the normalization of the work mechanism, effectively connect with the relevant work mechanisms of central departments, form a cooperative and coordinated working pattern between central and local governments, effectively prevent and properly handle risks related to virtual currencies and the tokenization of real-world assets, and maintain economic and financial order and social stability.

(5) Enhanced Risk Monitoring. The People's Bank of China, China Securities Regulatory Commission, National Development and Reform Commission, Ministry of Industry and Information Technology, Ministry of Public Security, State Administration of Foreign Exchange, Cyberspace Administration of China, and other departments continue to improve monitoring techniques and system support, enhance cross-departmental data analysis and sharing, establish sound information sharing and cross-validation mechanisms, promptly grasp the risk situation of activities related to virtual currency and real-world asset tokenization. Local governments at all levels give full play to the role of local monitoring and early warning mechanisms. Local financial regulatory authorities, together with branches and agencies of the State Council's financial regulatory authorities, as well as departments of cyberspace and public security, ensure effective connection between online monitoring, offline investigation, and fund tracking, efficiently and accurately identify activities related to virtual currency and real-world asset tokenization, promptly share risk information, improve early warning information dissemination, verification, and rapid response mechanisms.

(6) Strengthened Oversight of Financial Institutions, Intermediaries, and Technology Service Providers. Financial institutions (including non-bank payment institutions) are prohibited from providing account opening, fund transfer, and clearing services for virtual currency-related business activities, issuing and selling financial products related to virtual currency, including virtual currency and related financial products in the scope of collateral, conducting insurance business related to virtual currency, or including virtual currency in the scope of insurance liability. Financial institutions (including non-bank payment institutions) are prohibited from providing custody, clearing, and settlement services for unauthorized real-world asset tokenization-related business and related financial products. Relevant intermediary institutions and information technology service providers are prohibited from providing intermediary, technical, or other services for unauthorized real-world asset tokenization-related businesses and related financial products.

(7) Enhanced Management of Internet Information Content and Access. Internet enterprises are prohibited from providing online business venues, commercial displays, marketing, advertising, or paid traffic diversion services for virtual currency and real-world asset tokenization-related business activities. Upon discovering clues of illegal activities, they should promptly report to relevant departments and provide technical support and assistance for related investigations and inquiries. Based on the clues transferred by the financial regulatory authorities, the cyberspace administration, telecommunications authorities, and public security departments should promptly close and deal with websites, mobile applications (including mini-programs), and public accounts engaged in virtual currency and real-world asset tokenization-related business activities in accordance with the law.

(8) Strengthened Entity Registration and Advertisement Management. Market supervision departments strengthen entity registration and management, and enterprise and individual business registrations must not contain terms such as "virtual currency," "virtual asset," "cryptocurrency," "crypto asset," "stablecoin," "real-world asset tokenization," or "RWA" in their names or business scopes. Market supervision departments, together with financial regulatory authorities, legally enhance the supervision of advertisements related to virtual currency and real-world asset tokenization, promptly investigating and handling relevant illegal advertisements.

(IX) Continued Rectification of Virtual Currency Mining Activities. The National Development and Reform Commission, together with relevant departments, strictly controls virtual currency mining activities, continuously promotes the rectification of virtual currency mining activities. The people's governments of various provinces take overall responsibility for the rectification of "mining" within their respective administrative regions. In accordance with the requirements of the National Development and Reform Commission and other departments in the "Notice on the Rectification of Virtual Currency Mining Activities" (NDRC Energy-saving Building [2021] No. 1283) and the provisions of the "Guidance Catalog for Industrial Structure Adjustment (2024 Edition)," a comprehensive review, investigation, and closure of existing virtual currency mining projects are conducted, new mining projects are strictly prohibited, and mining machine production enterprises are strictly prohibited from providing mining machine sales and other services within the country.

(X) Severe Crackdown on Related Illegal Financial Activities. Upon discovering clues to illegal financial activities related to virtual currency and the tokenization of real-world assets, local financial regulatory authorities, branches of the State Council's financial regulatory authorities, and other relevant departments promptly investigate, determine, and properly handle the issues in accordance with the law, and seriously hold the relevant entities and individuals legally responsible. Those suspected of crimes are transferred to the judicial authorities for processing according to the law.

(XI) Severe Crackdown on Related Illegal and Criminal Activities. The Ministry of Public Security, the People's Bank of China, the State Administration for Market Regulation, the China Banking and Insurance Regulatory Commission, the China Securities Regulatory Commission, as well as judicial and procuratorial organs, in accordance with their respective responsibilities, rigorously crack down on illegal and criminal activities related to virtual currency, the tokenization of real-world assets, such as fraud, money laundering, illegal business operations, pyramid schemes, illegal fundraising, and other illegal and criminal activities carried out under the guise of virtual currency, the tokenization of real-world assets, etc.

(XII) Strengthen Industry Self-discipline. Relevant industry associations should enhance membership management and policy advocacy, based on their own responsibilities, advocate and urge member units to resist illegal financial activities related to virtual currency and the tokenization of real-world assets. Member units that violate regulatory policies and industry self-discipline rules are to be disciplined in accordance with relevant self-regulatory management regulations. By leveraging various industry infrastructure, conduct risk monitoring related to virtual currency, the tokenization of real-world assets, and promptly transfer issue clues to relevant departments.

(XIII) Without the approval of relevant departments in accordance with the law and regulations, domestic entities and foreign entities controlled by them may not issue virtual currency overseas.

(XIV) Domestic entities engaging directly or indirectly in overseas external debt-based tokenization of real-world assets, or conducting asset securitization activities abroad based on domestic ownership rights, income rights, etc. (hereinafter referred to as domestic equity), should be strictly regulated in accordance with the principles of "same business, same risk, same rules." The National Development and Reform Commission, the China Securities Regulatory Commission, the State Administration of Foreign Exchange, and other relevant departments regulate it according to their respective responsibilities. For other forms of overseas real-world asset tokenization activities based on domestic equity by domestic entities, the China Securities Regulatory Commission, together with relevant departments, supervise according to their division of responsibilities. Without the consent and filing of relevant departments, no unit or individual may engage in the above-mentioned business.

(15) Overseas subsidiaries and branches of domestic financial institutions providing Real World Asset Tokenization-related services overseas shall do so legally and prudently. They shall have professional personnel and systems in place to effectively mitigate business risks, strictly implement customer onboarding, suitability management, anti-money laundering requirements, and incorporate them into the domestic financial institutions' compliance and risk management system. Intermediaries and information technology service providers offering Real World Asset Tokenization services abroad based on domestic equity or conducting Real World Asset Tokenization business in the form of overseas debt for domestic entities directly or indirectly venturing abroad must strictly comply with relevant laws and regulations. They should establish and improve relevant compliance and internal control systems in accordance with relevant normative requirements, strengthen business and risk control, and report the business developments to the relevant regulatory authorities for approval or filing.

(16) Strengthen organizational leadership and overall coordination. All departments and regions should attach great importance to the prevention of risks related to virtual currencies and Real World Asset Tokenization, strengthen organizational leadership, clarify work responsibilities, form a long-term effective working mechanism with centralized coordination, local implementation, and shared responsibilities, maintain high pressure, dynamically monitor risks, effectively prevent and mitigate risks in an orderly and efficient manner, legally protect the property security of the people, and make every effort to maintain economic and financial order and social stability.

(17) Widely carry out publicity and education. All departments, regions, and industry associations should make full use of various media and other communication channels to disseminate information through legal and policy interpretation, analysis of typical cases, and education on investment risks, etc. They should promote the illegality and harm of virtual currencies and Real World Asset Tokenization-related businesses and their manifestations, fully alert to potential risks and hidden dangers, and enhance public awareness and identification capabilities for risk prevention.

(18) Engaging in illegal financial activities related to virtual currencies and Real World Asset Tokenization in violation of this notice, as well as providing services for virtual currencies and Real World Asset Tokenization-related businesses, shall be punished in accordance with relevant regulations. If it constitutes a crime, criminal liability shall be pursued according to the law. For domestic entities and individuals who knowingly or should have known that overseas entities illegally provided virtual currency or Real World Asset Tokenization-related services to domestic entities and still assisted them, relevant responsibilities shall be pursued according to the law. If it constitutes a crime, criminal liability shall be pursued according to the law.

(19) If any unit or individual invests in virtual currencies, Real World Asset Tokens, and related financial products against public order and good customs, the relevant civil legal actions shall be invalid, and any resulting losses shall be borne by them. If there are suspicions of disrupting financial order and jeopardizing financial security, the relevant departments shall deal with them according to the law.

This notice shall enter into force upon the date of its issuance. The People's Bank of China and ten other departments' "Notice on Further Preventing and Dealing with the Risks of Virtual Currency Trading Speculation" (Yinfa [2021] No. 237) is hereby repealed.

Former Partner's Perspective on Multicoin: Kyle's Exit, But the Game He Left Behind Just Getting Started

Why Bitcoin Is Falling Now: The Real Reasons Behind BTC's Crash & WEEX's Smart Profit Playbook

Bitcoin's ongoing crash explained: Discover the 5 hidden triggers behind BTC's plunge & how WEEX's Auto Earn and Trade to Earn strategies help traders profit from crypto market volatility.